UK: New research from Bidwells reveals the UK’s operational living sector is facing a period of significant challenge, with BTR particularly badly affected – BTR planning applications have fallen to their lowest level since 2015 and current submissions are 35 per cent below the 10-year average.

The UK operational living sector has experienced a sustained decline in planning activity over the past 18 to 24 months, threatening to cause a significant supply reduction in the coming years with a lack of stock entering the pipeline. While this undersupply challenge may appear some way off, it is already taking shape and is likely to become more acute in the coming years, with knock-on effects for the wider UK economy and housing market.

Bidwells Operational Living analysis reveals that, between 2014 and 2022, there were around 57 planning application submissions for multi-family Build to Rent developments nationwide per annum. Since 2022, submissions have started to fall – with 2024 recording the lowest number of MF BTR planning submissions since 2015. In 2025 so far, planning submissions are 35 per cent below the ten-year average.

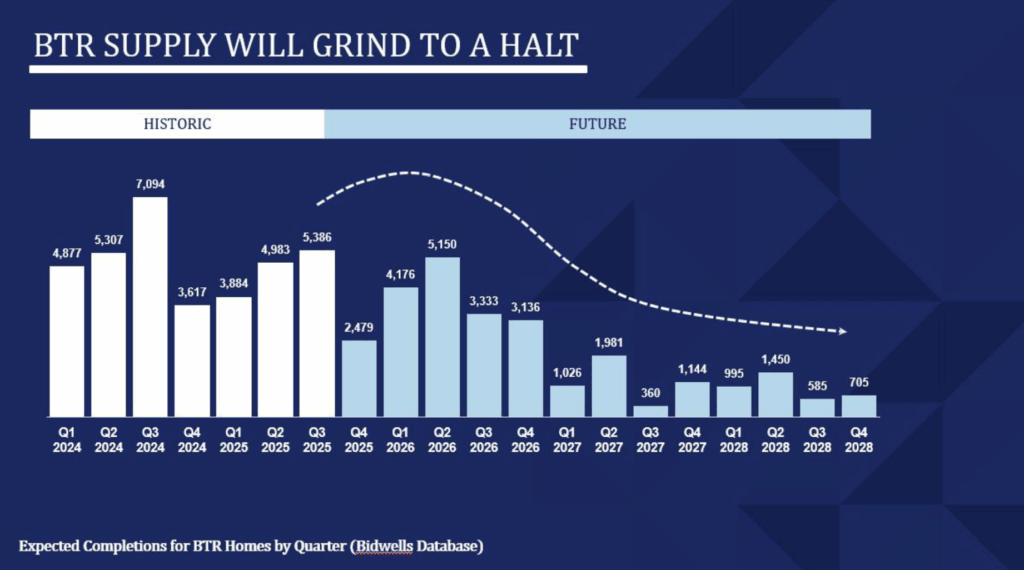

Whilst the introduction of the Building Safety Act (2022), rising inflation, and construction costs have clearly impacted the number of starts across the UK, the decline in planning applications is placing significant strain on the future rental and investment markets, as fewer projects are entering the pipeline to drive growth. We are already seeing the knock-on effects of this, with a sharp drop in expected completions beyond Q1 2027.

Between Q1 2027 and Q4 2028, only 8,246 BTR, single-family and co-living homes are projected to complete, compared with 32,527 between 2025 and 2026. This slowdown in delivery will disrupt the supply schedule and create a pronounced undersupply of operational living stock. With demand for BTR and related sectors continuing to grow, the imbalance is likely to put upward pressure on rents, reducing affordability for many residents and further challenging market viability.

We predict that this will create a dramatic slow-down in BTR supply. Concerningly, by 2028, we predict supply will be 82% lower than in 2024 – with just 3,735 BTR homes delivered that year, compared to 20,895 in 2024.

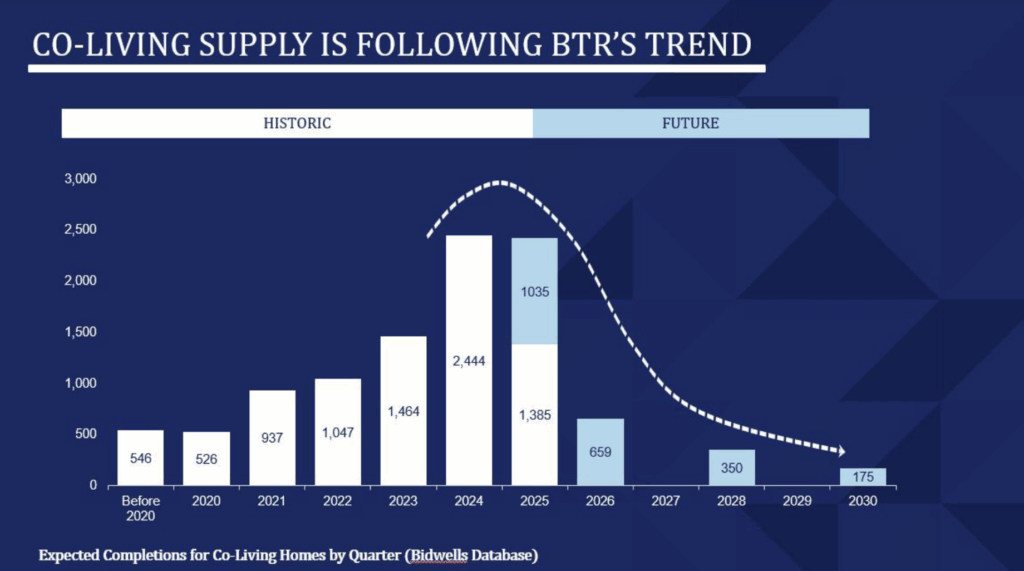

Coliving, a sub-sector of Build to Rent, is projected to deliver just 1,184 new homes between 2026 and 2030. This is fewer than the 1,385 delivered in the first three quarters of 2025 alone, marking a significant slowdown on the horizon.

Our research reveals over 12,600 BTR homes in London that have planning permission but are yet to start construction, alongside over 8,100 co-living homes. Outside London, there are over 38,200 BTR homes with unactioned planning permission, and over 7,000 co-living homes. A significant block therefore exists in the post-planning development pipeline which threatens to seriously affect the UK’s residential market which could stifle future economic growth.

This extends into other sectors too. For instance, PBSA (Purpose-Built Student Accommodation) applications in 2025 so far have fallen by 54 per cent against the 2020–2024 average. But while coliving supply is showing signs of a slow-down, there is some hope for this sector. Coliving planning application submissions have totalled 17 so far in 2025 (Q1-Q3), with evidence of this rising steadily, signalling continued investor interest. In 2018 and 2019, there were just four applications submitted between Q1 and Q3, rising to 12 in 2022 and 2023, and 16 in 2024. 17 in 2025 marks a new record high.

The slow-down in Build to Rent is representative of a wider slow-down across the residential development sector currently. Caused by several macro-factors, among them high interest rates and increased regulation brought about through the Building Safety Act. According to the ONS, planning applications for all new dwellings across the UK fell from a 10-year high of 182,000 in 2022 to just 107,000 in 2024. While Q1 2025 (the latest data) shows a slight rebound, 2024 and 2025 are set to be the slowest years for planning application submissions since the 2008 Financial Crash. This poses a significant risk to the government’s plan to deliver 1.5 million homes within this parliament.

My favourite analogy: “If we don’t put sausage meat in the sausage machine, we won’t get sausages.”

With gilt yields rising sharply, 10-year government bonds climbing above 4.8 per cent in early September and 30-year yields reaching 5.7 per cent — the highest level since 1997. These higher yields are driving up the cost of borrowing and, given their zero-risk status, setting a benchmark return for investors. As a result, property sectors such as Operational Living, including BTR, are becoming relatively less attractive, limiting new investment and further slowing growth across the sector.

According to the Planning London Datahub, residential starts across the wider market are reflecting the same slowdown evident in Operational Living. From 2024 to August 2025, only 9,539 flat and apartment maisonette starts have been recorded, compared with an average of 43,848 starts per year between 2015 and 2023 and 22,980 starts in 2023/2024 alone. This represents a dramatic decline in delivery and highlights the growing challenges in bringing new homes in this asset class to fruition.

We are also seeing hundreds of homes empty across the UK due to Gateway 3. There are 1,210 completed homes which cannot be occupied due to delays of the Building Safety Regulator, with an additional 34,965 new homes listed as “no decision” across 156 applications. Gateway 3 is now creating situations where completed homes cannot be occupied. This is an emerging issue that so far has received little attention but carries significant implications for housing delivery. New buildings are intended to be signed off within 12 weeks, however, there are reports that the proportion of applications determined within this timeframe have declined, from 47 per cent this time last year to just 32 per cent by the end of March 2025.

Jon Spring, managing director of Fairview Homes, warned that delays risk making projects unviable. He explained that if each scheme takes 25 per cent longer to deliver, productivity falls by the same margin — a challenge facing all developers, which could result in a significant reduction in the volume of housing delivered*

But demand continues

The UK’s housing market is now caught in a vicious spiral. A chronic shortage of homes, festering for decades, has erupted into a full-blown crisis. Instead of ramping up construction to meet urgent demand, supply is collapsing – and with every home that isn’t built, rents surge higher still. The result: a relentless squeeze on millions of households, as the cost of simply having a roof over one’s head continues to soar.

Rental values are growing in double digits across all core cities. Edinburgh has led the way, with apartment rents rising the most, while Brighton recorded the lowest increase in the low-to-mid single digits. This sustained growth highlights strong and ongoing demand for rental housing. However, if supply begins to fall, the market will tighten further, pushing rents higher and potentially narrowing the pool of residents able to access Build-to-Rent homes.

With rental demand across the UK remaining strong and supply slowing, investors are increasingly targeting stabilised assets that offer the potential for outsized returns. While transactions are limited, at least one £1 billion-plus deal is currently in play, with more expected to follow. Despite reduced deal flow, high-quality stabilised assets trading at or below replacement cost continue to attract capital, viewed as resilient long-term opportunities in an otherwise challenging market.

These secondary trades in the BTR market signal a maturing market. While new development has slowed significantly, these transactions provide valuable benchmarks on exit pricing, which can help give developers the confidence to bring forward new schemes.

The Build-to-Rent Alliance has launched by the British Property Federation and Association for Rental Living against a backdrop of slowing BTR delivery across all UK regions, with mounting policy and regulatory challenges making it harder to bring forward new schemes and threatening to erode investor confidence.

The Alliance has been founded to set out two immediate priorities: first, to advocate for the policy and regulatory changes needed to restore investor confidence and address viability and delivery challenges; and second, to improve the consumer experience and perception of Build-to-Rent (BTR) within the private rented sector, positioning it as a tenure of first choice. A new Consumer Code will be central to achieving this.

The timing is significant. Bidwells Operational Living analysis shows completions of new BTR developments have outpaced planning applications submitted for six consecutive quarters. Highlighting a continued lull in the operational living pipeline.

The data also underlines the growing impact of delays at the Building Safety Regulator (BSR), which are increasingly holding back BTR delivery. Combined with wider viability pressures, these factors are beginning to cool investment sentiment in a sector once seen as transformative for housing supply.

Against this backdrop, the Alliance will work to raise awareness among local authorities of the benefits of BTR and press for a more supportive environment that enables new schemes to come forward. Whilst this is a positive step in the right direction, there is more that we can be doing in the sector in order to facilitate this further and drive growth in the sector.

Summary:

The UK’s Build to Rent (BTR) sector is facing a period of significant challenge, with planning applications falling to their lowest level since 2015 and current submissions 35 per cent below the ten-year average. This decline, coupled with regulatory delays linked to the Building Safety Act and the Gateways, is creating a substantial blockage in the pipeline and slowing delivery across the country. Projections show a sharp drop in expected completions, with supply anticipated to fall by 82 per cent between 2024 and 2028, posing a serious risk to meeting demand. At the same time, rental demand remains strong, with double-digit rent growth in many cities, further straining affordability. In response, investor focus is shifting toward stabilised assets, highlighting a maturing but supply-constrained market. To address these issues, the Build to Rent Alliance has been launched, advocating for policy reform to restore investor confidence and strengthen consumer protections, but further action will be required to ensure growth in the sector continues.

This article was a Bidwells Operational Living team collaboration between Iain Murray, Head of Operational Living, Ed Howe, Head of BTR Research and Hamish Owen, Graduate Operational Living Analyst at Bidwells.

*Sky News (02/09/2025) – https://news.sky.com/story/the-red-tape-keeping-these-flats-empty-and-threatening-labours-vital-new-homes-target-13423446